What is CORSIA and why is it important?

September 15, 2025 - Research

CORSIA, or the Carbon Offsetting and Reduction Scheme for International Aviation, is a global plan to reduce carbon emissions from international flights. Adopted by the International Civil Aviation Organization (ICAO) in 2016, CORSIA requires airlines to keep their emissions from international flights below 85% of their 2019 levels using eligible sustainable aviation fuel (SAF) and/or eligible carbon credits.

CORSIA consists of three distinct phases based on compliance periods:

- Pilot Phase (2021 to 2023)

- First Phase (2024 to 2026)

- Second Phase (2027 to 2035)

Some sources estimate that demand for First Phase carbon credits may be up to 160 million tonnes of CO2e. However, today’s supply of such carbon credits is very limited. Only a handful of projects have issued First Phase-eligible credits.

ICAO requires host countries to agree that carbon credits used by airlines to meet CORSIA obligations be accounted for under the host country’s Paris Agreement target, referred to as “Nationally Determined Contributions (NDCs).” These units must carry host party authorization and a corresponding adjustment so they are not also counted toward the host’s NDC.

Are CORSIA credits high-quality?

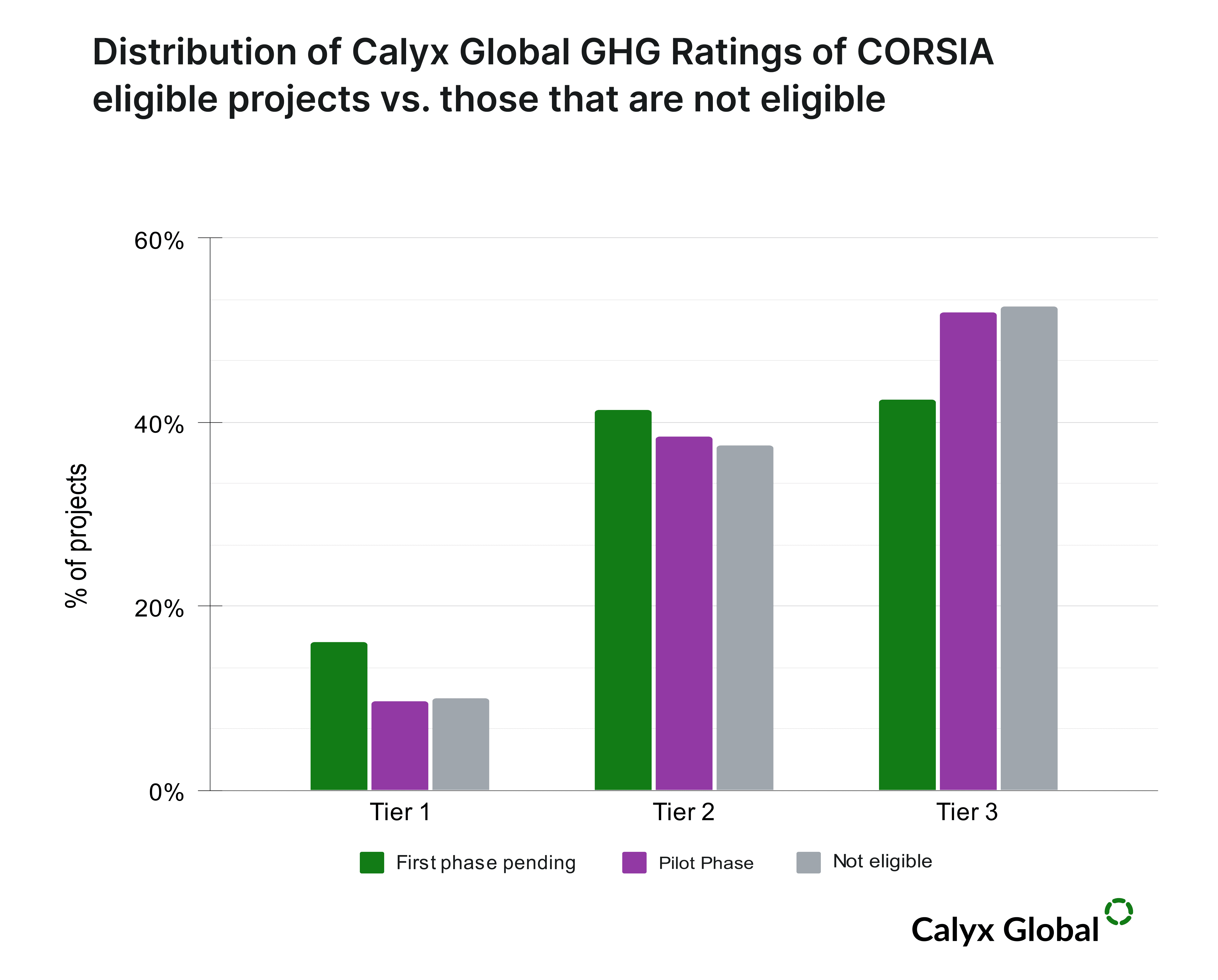

In general, CORSIA eligibility is not a strong indicator of GHG integrity for carbon credits. The ICAO relies on recommendations from the Technical Advisory Body (TAB), which applies broad criteria to carbon crediting programs, with a few exclusions for certain project types. Our analysis suggests that this blunt tool does not sort high from low quality well. The graph below indicates that CORSIA’s First Phase credits appear to boast slightly higher GHG integrity on average than carbon credits that are ineligible or Pilot Phase-eligible. However, regardless of phase, the quality of most CORSIA-eligible credits is still low, landing in our Tier 2 and 3 categories.

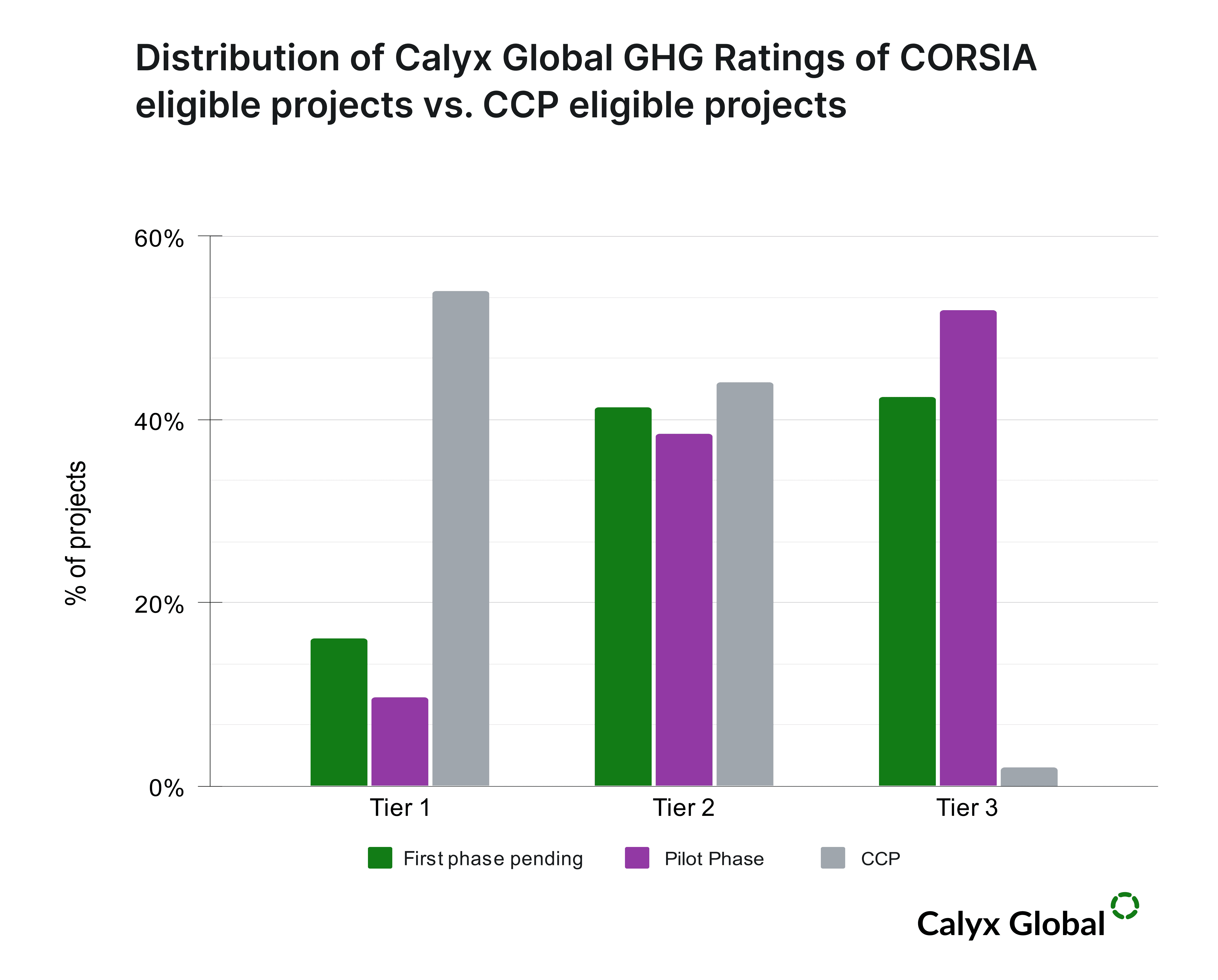

By contrast, the Integrity Council for the Voluntary Carbon Market’s (ICVCM’s) Core Carbon Principle (CCP) label is a stronger indicator of credit quality. The image below illustrates the difference in quality between ICVCM CCP and CORSIA eligibility. That said, CCP-eligible credits still can exhibit material risks (i.e., be in the Calyx Global Tier 2 or 3 categories).

Despite the somewhat disappointing quality signal of CORSIA-eligibility, these carbon credits will still be essential for airlines to meet compliance goals over the next several years. The good news is that there are high GHG integrity credits out there that may be eligible for CORSIA – one just needs to know where to look.

What type of credits are CORSIA-eligible?

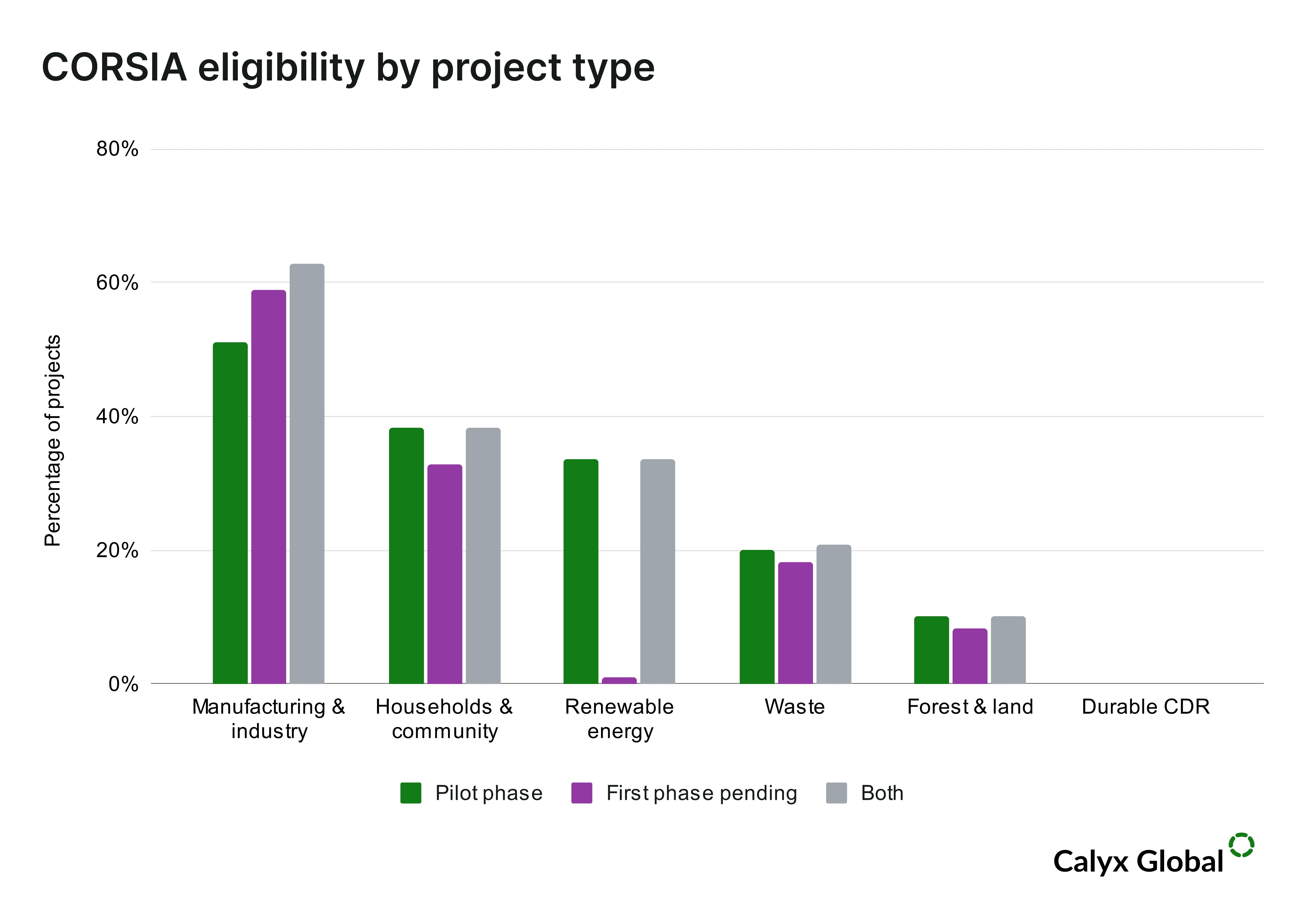

ICAO’s Eligible Emissions Units (EEU) criteria contain several restrictions and exclusions that prevent certain project types from obtaining CORSIA eligibility as frequently as other project types. It is therefore important to understand which project types are most often eligible. The graph below indicates the percentage of credits rated by Calyx Global under each project type category that are eligible for the Pilot and First Phase of CORSIA (pending host country authorization).

Currently, the only source of CORSIA First Phase-eligible credits comes from one jurisdictional REDD (J-REDD) program: Guyana. This program has the benefit of receiving host country approval for use under CORSIA. All other sources are only fully eligible for the First Phase pending host country approval, the requirements for which differ from program to program.

Calyx Global has rated this program and it, unfortunately, falls into our Tier 3 category. Guyana is a special case of J-REDD as it falls into the “high forest cover, low deforestation” (HFLD) category under ART-TREES, which allows the country to apply special provisions to increase its crediting baseline. These provisions seek to acknowledge the significant role these jurisdictions have played historically in preserving critical forests and the challenges they face to benefit from carbon markets under traditional methodologies. However, such baselines are controversial and may be why the ICVCM has not yet approved HFLD approaches to date.

The graph above suggests that the category producing the highest percentage of projects able to generate CORSIA-eligible credits is manufacturing and industry. These include the destruction of ozone-depleting substances (ODS) or abatement of nitrous oxide (N2O). This is followed by the category of households and community projects (cookstoves, household biodigesters, etc.). These project types generally have fewer eligibility restrictions than others.

Manufacturing & industry credits vs. household and community credits

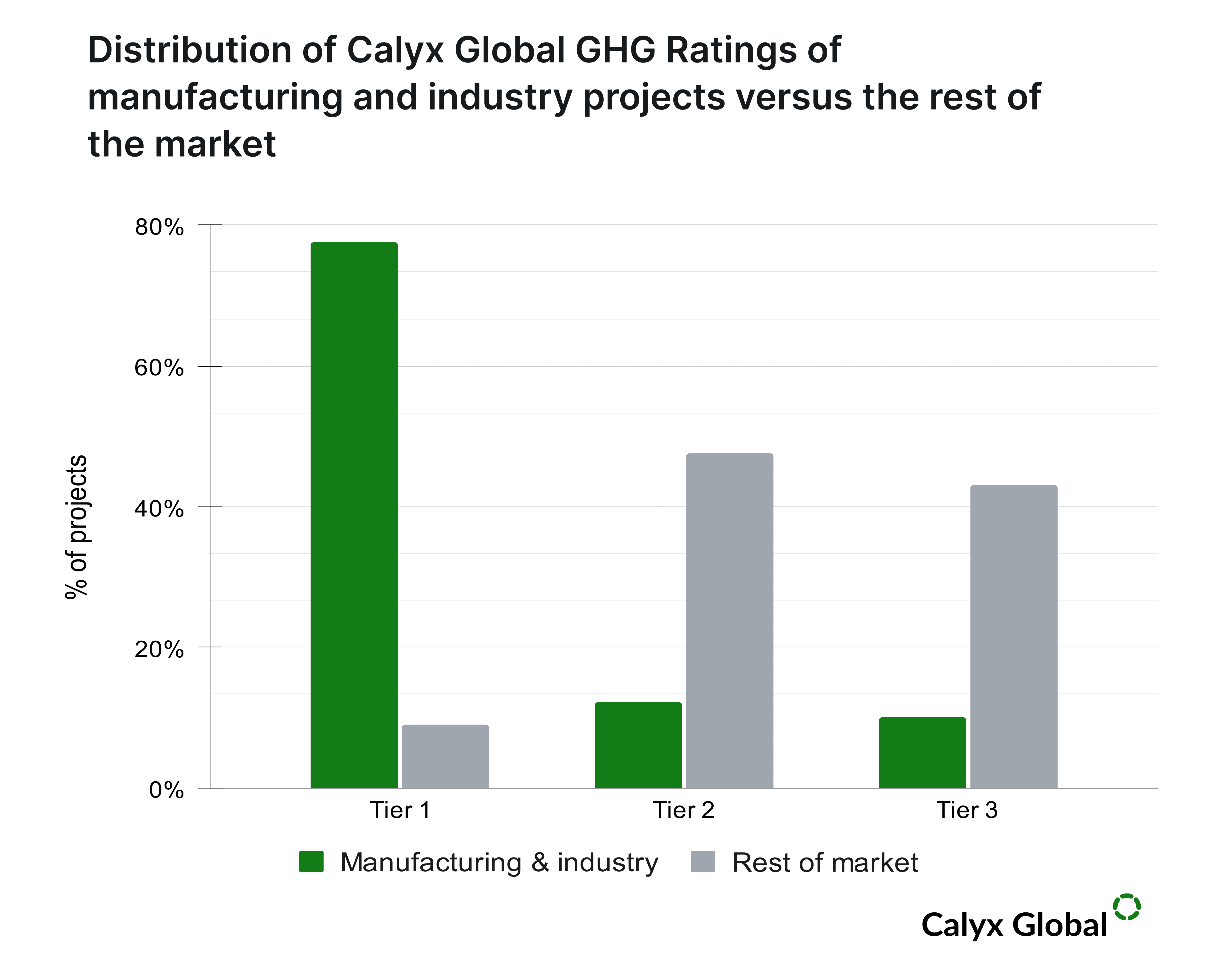

Not only are manufacturing and industry projects more likely to produce CORSIA-eligible credits, but they are also some of the highest-quality credits in the VCM. The graph below shows that these credits tend to boast significantly higher GHG-integrity compared to the rest of the market. This suggests that manufacturing and industry projects may prove to be a source of high-quality, CORSIA-eligible carbon credits. Most of these projects represent “super pollutant” mitigation, i.e., the abatement of high global warming greenhouse gases (as opposed to CO2).

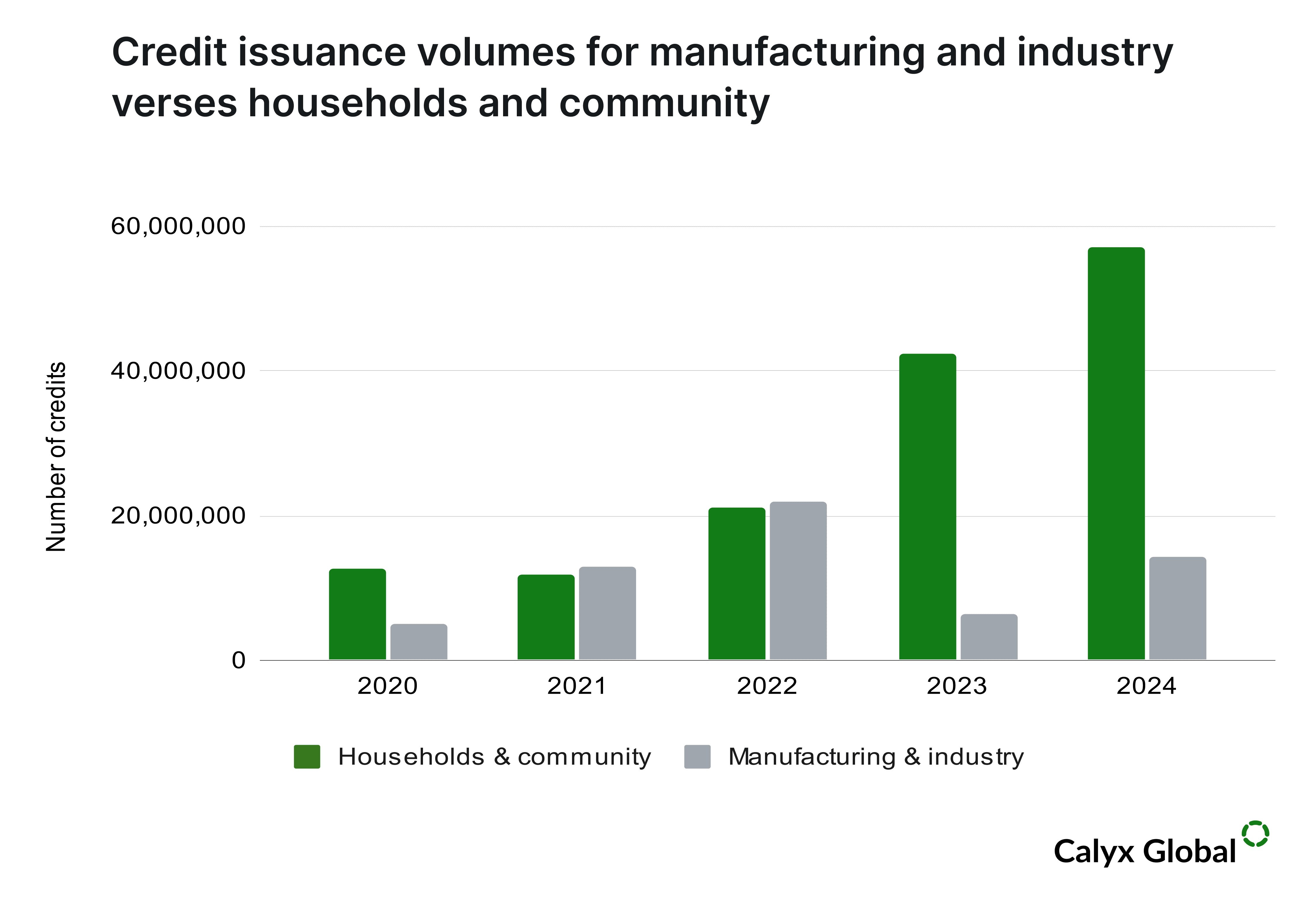

However, the supply of credits from manufacturing and industry projects will not be able to meet expected CORSIA demand unless there is an acceleration in the development of such projects. By contrast, household and community projects currently generate higher volumes of credits, but cannot claim the same level of GHG-integrity. This is in large part due to over-crediting issues. The graph below shows recent credit issuance volumes of these two categories.

Over the last few years, cookstoves and other household and community project types have seen a significant spike in issuance volumes. In 2024, household and community projects generated around four times as many credits as manufacturing and industry projects. As noted above, most of the key risk drivers associated with household and community projects revolve around over-crediting. In our recent blog post “Cooking up Quality: Carbon credits from efficient cookstove projects face integrity issues worth fixing”, we discuss steps that can and are being taken to improve the GHG integrity of these projects. As such, they should not be discounted as a key source of EEUs – but may not provide as many high-quality credits as the above graph suggests, as improvement to GHG integrity of these projects will require projects to lower the number of credits they can issue.

SDG benefits of manufacturing and industry projects vs household and community projects

Manufacturing and industry and household and community projects contribute to Sustainable Development in different and complementary ways. Manufacturing and industry projects advance sustainable innovation (SDG 9) through cleaner technologies, improving resource efficiency and reducing pollution for responsible consumption and production (SDG 12). By lowering harmful emissions or even reducing ozone depletion, these efforts also contribute to health and well-being (SDG 3).

Household and community projects directly benefit households and communities by lowering biomass use, leading to savings (SDG 1) and improved health from reduced indoor air pollution (SDG 3). This also promotes sustainable resource use (SDG 12), benefiting local ecosystems and biodiversity (SDG 15). Furthermore, these projects boost local economies by creating jobs (SDG 8) that utilize and build local skills for technologies like cookstoves, biodigesters and off-grid solar.

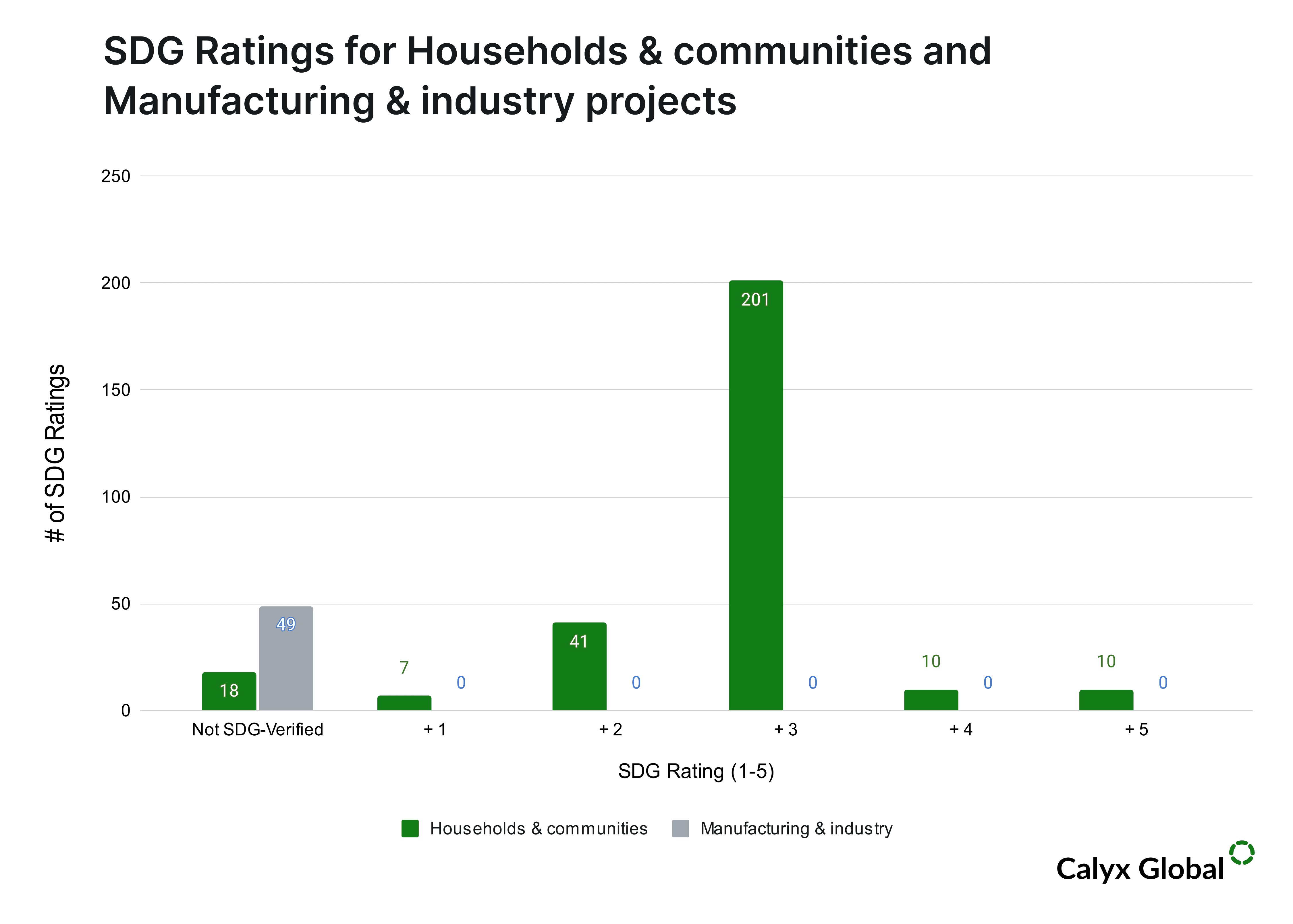

The picture looks different when viewing SDG Ratings through the project lens instead of credits. Note that Calyx Global’s SDG ratings only cover verified SDG contributions (see Verified SDG contributions vs. self-claimed). To date, there is a stark contrast between manufacturing and industry, which have no projects with SDG certification due to their crediting programs, and household and community projects, which are largely SDG-certified.

Both project types play complementary roles in fostering sustainable development. As the market evolves, SDG certification can contribute to boosting the profile of manufacturing and industry projects.

Conclusion

To meet CORSIA goals and drive sustainable development, both manufacturing and industry projects and household and community projects are needed.

Together, these project types have the potential to generate significant volumes of higher-quality EEUs. Stay tuned as we continue to monitor CORSIA eligibility trends. View CORSIA eligible credits on the Calyx Global Platform for free by filtering for “CORSIA.”

Keep up with carbon market trends

Get the monthly newsletter and stay in the loop.

Trusted By