How deferred accounting undermines the quality of CDR credits

August 21, 2025 - Research

Carbon dioxide removal (CDR) is embedded in all pathways that limit global warming to 1.5 or 2℃. The voluntary carbon market is helping to drive innovation in CDR – from technologies, to financing models and basic science that supports better measurement of removals. Interest in engineered CDR, such as direct air capture (DAC) and biomass carbon removal and storage (BiCRS), is growing rapidly. Purchase agreements for future delivery of engineered CDR grew sevenfold from 2022 to 2023, and nearly doubled to 8.2 million credits in 2024. Another 25 million credits have already been purchased since the beginning of 2025, largely driven by Microsoft.

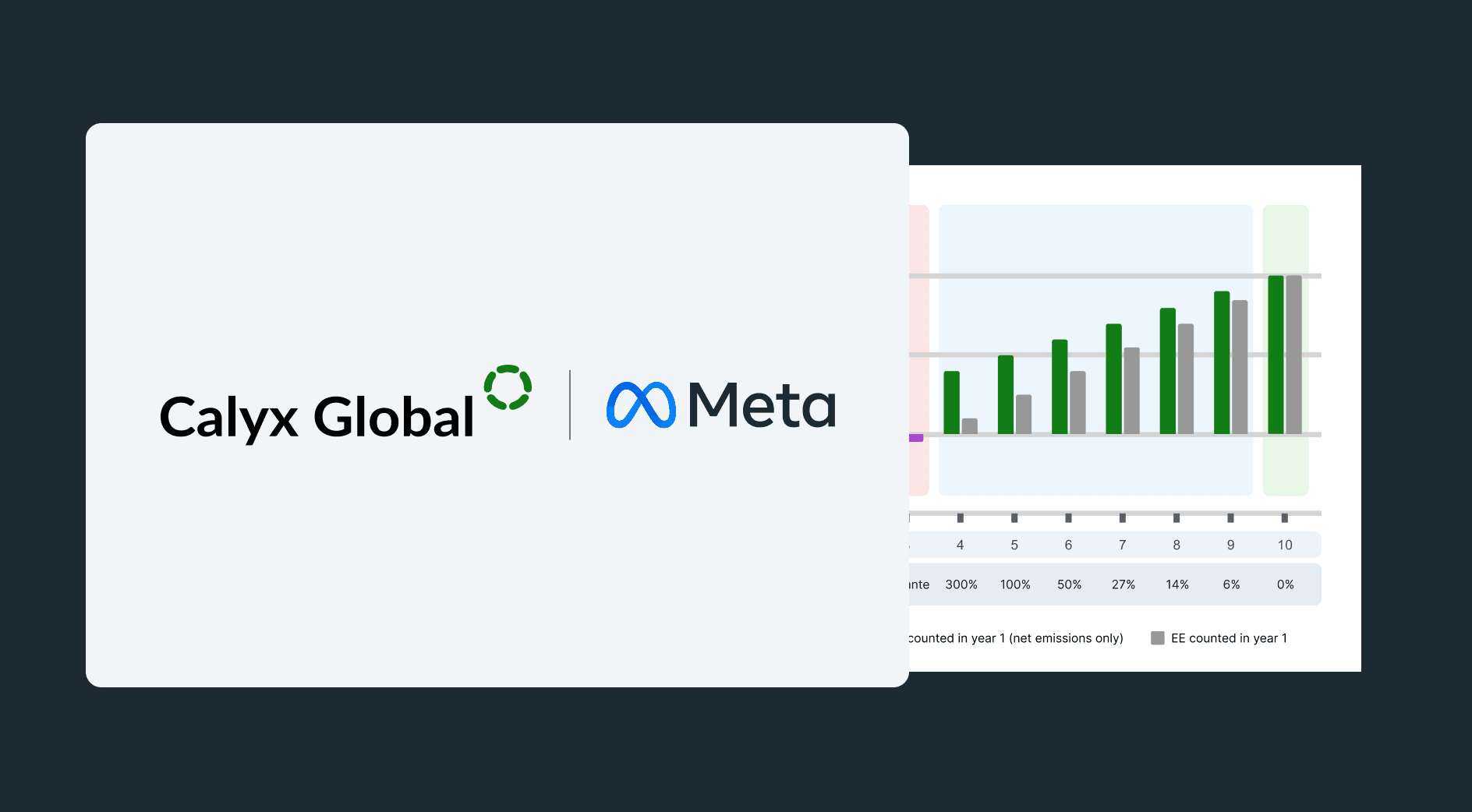

One critical issue across CDR projects is the proper accounting of “embodied emissions” – the emissions associated with the construction, maintenance and eventual decommissioning of infrastructure. The upfront embodied emissions, or those occurring before the project starts to remove CO2, create a debt that must be paid off before a project delivers a net climate benefit. However, many carbon accounting methodologies either ignore these emissions or allow them to be spread out over years, rather than deducted upfront, when they occur.

Amortizing upfront embodied emissions can lead to ex-ante crediting – issuing credits before a project has delivered real atmospheric benefit. Even in more optimistic scenarios, where the project operates as planned and eventually pays off its emissions debt, amortization still overstates the climate benefit until that amortization is complete. During this period, each credit issued claims more carbon removed than has actually occurred, meaning that a portion of each credit is not yet backed by real CO2 removal.

This matters if the credit is being used to offset emissions – such as a company claiming net zero after retiring a CDR credit. In such cases, removal credits ostensibly have neutralized the company’s emissions. However, because the CDR credit is, in whole or part, a promise of future removal, the company’s emissions have actually not (yet) been neutralized. If the project ends prematurely, for financial, technical or other reasons, the promised removal may never materialize, undermining both climate impact and trust in carbon markets.

To ensure CDR credits reflect real climate impact, two key practices are recommended:

- Account for embodied emissions upfront. These emissions are committed at project initiation and should be deducted from removals before credits are issued.

- Mandate transparency in emissions reporting. Buyers and stakeholders must be able to see full lifecycle emissions – including upstream (construction), operational and downstream (decommissioning) – in order to assess when a project delivers net removals. To the extent that emissions are amortized, a clear designation that allows buyers to understand the remaining carbon debt and to make informed decisions about use and claims associated with these credits is vital. Especially during a transition from the current approach that permits ex-ante crediting, projects that account upfront for embodied emissions should receive a designation that allows a buyer to know that such credits represent a full tonne of removal at the time of issuance.

The engineered CDR market is scaling quickly. Now is the time to set rigorous, standardized accounting practices to ensure integrity, avoid over-crediting and build lasting trust in CDR as a climate solution.

To dive deeper into embodied emissions accounting and its impact on engineered CDR projects, read the paper from Meta and Calyx Global.

Keep up with carbon market trends

Get the monthly newsletter and stay in the loop.

Trusted By